Well thank you Santa!! With all of the negative economic news in the last few weeks, we have to remember (sadly) that bad news for the Economy is good news for Mortgage Rates. This has all led to the Bank of Canada holding firm for the third consecutive meeting and leads us to strongly believe that the fever will break sooner than expected in 2024.

Some cookies to crumble: Remember that FIXED RATES and VARIABLE RATES move at DIFFERENT TIMES. Many believe that rates ONLY move when the Bank of Canada meet, this is absolutely NOT TRUE. Whilst the Prime Rate does move with the Bank of Canada announcements, the discount from those rates can move any day of the week. FIXED RATES have already been coming steadily down over the last week or so and we are starting to see a light at the end of the tunnel.

A few fairy lights to ponder over: OFSI the Regulator also recently announced that if a Borrower is SWITCHING their mortgage with no new funds then they do NOT need to stress test. This has most definitely held Borrowers back this year from switching Lenders, and Lenders knew that! They were deliberately quoting HIGH renewal rates simply because they knew clients couldn’t go elsewhere. Do NOT sign that renewal letter. Your current Lender does NOT have your best interests at heart, they just want to earn top dollar. Let us at least review that letter for you.

Has Rudolph eaten too many carrots? Many many clients have found themselves in hot water with high balances on credit cards and lines of credit. We are seeing rates anywhere between 19-24% and this is very painful. Remember, property values have increased over these last number of years, do not be afraid to make that Equity WORK for you. That is what YOU worked hard for. We have been able to ease cashflow and debt for many of our clients this year and we expect that to continue. We have all seen that pain personally. It just takes an expert understanding of how to make the books balance again. Please do reach out.

As always, our Team is here to talk you through all options.

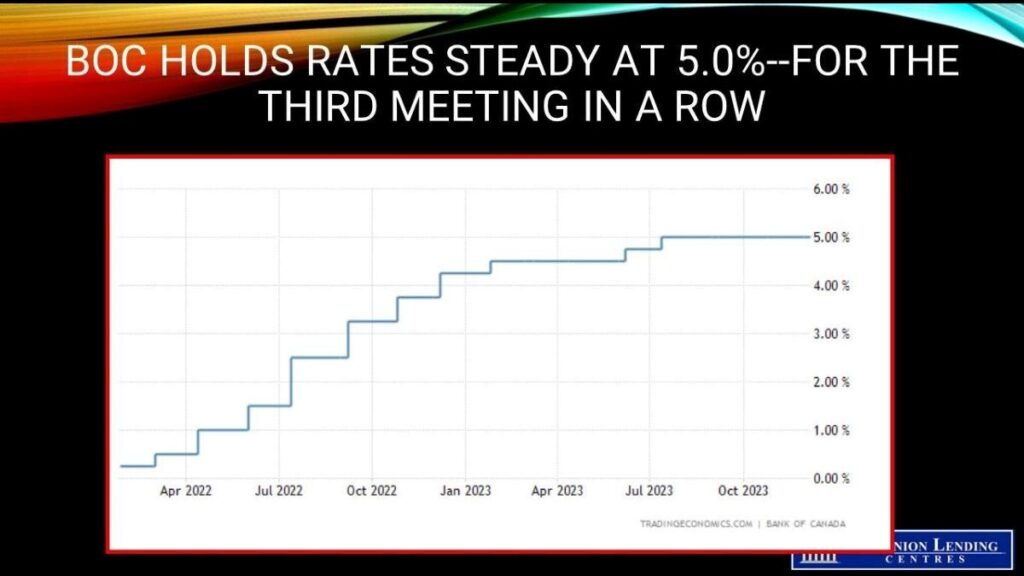

The Bank of Canada held rates steady once again, and the press release took a more neutral tone–commenting that the economy and labour markets have slowed and inflation has fallen.

The Bank of Canada Held Rates Steady and Took A More Neutral Tone

It was widely expected that the Bank of Canada would maintain its key policy rate at 5% for the third consecutive time. It will continue to sell government securities (quantitative tightening) to normalize its balance sheet. Market participants weighed and measured each word of the BoC press release and assessed that the Bank took a less hawkish stance.

This time, the release said, “Higher interest rates are clearly restraining spending: consumption growth in the last two quarters was close to zero, and business investment has been volatile but essentially flat over the past year. Exports and inventory adjustment subtracted from GDP growth in the third quarter, while government spending and new home construction provided a boost. The labour market continues to ease: job creation has been slower than labour force growth, job vacancies have declined further, and the unemployment rate has risen modestly. Even so, wages are still rising by 4-5%. Overall, these data and indicators for the fourth quarter suggest the economy is no longer in excess demand.”

At the prior meeting in late October, the Bank said that the labour market remained “on the tight side” but acknowledged today that it was loosening. Indeed, the October Monetary Policy Report suggested that the inflation rate would not hit its 2% target level until late 2025.

Today, the tone was much more optimistic, suggesting that policymakers are increasingly confident interest rates are restrictive enough to bring inflation back to the 2% target. Still, Bank officials want to see more progress on core inflation before it begins to ease. It said, “The Bank’s preferred measures of core inflation have been around 3½-4%, with the October data coming in towards the lower end of this range.”

The central bank focuses on “the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour” and remains resolute in restoring price stability.

Bottom Line

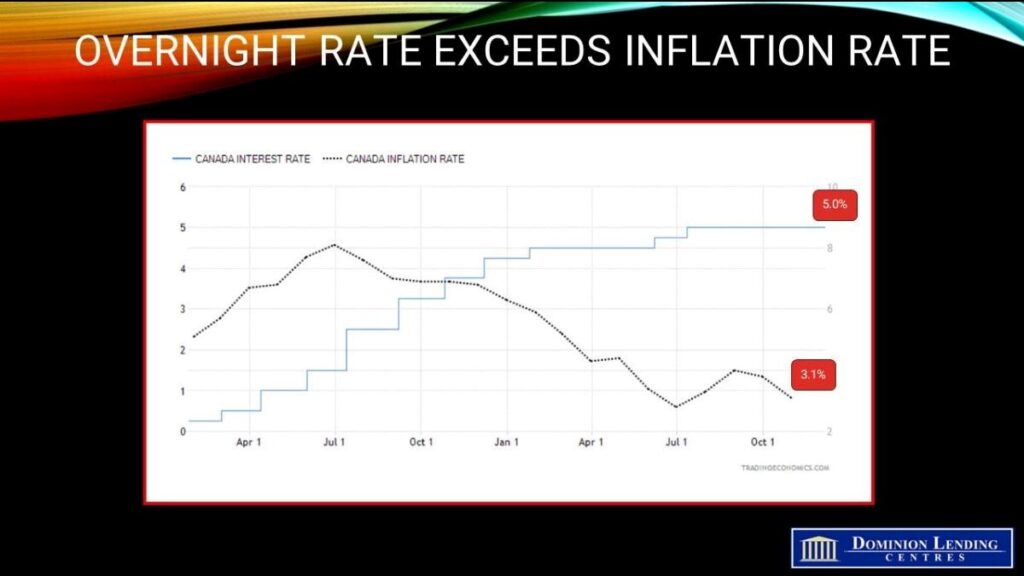

Bond yields peaked in early October and have fallen by nearly 100 basis points. This has led to reductions in fixed mortgage rates; however, those cuts have been far less than historical experience would have suggested, given the rally in 5-year government bonds.

Cuts in variable mortgage rates await a reduction in the overnight policy rate, which triggers a commensurate decline in the prime rate, which is currently stuck at 7.2%. I expect the BoC to begin cutting the policy rate by the middle of next year, taking it down a full percentage point to 4% by yearend.

Dr. Sherry Cooper

Chief Economist, Dominion Lending Centres

drsherrycooper@dominionlending.ca

0 Comments